How the UAE Open Finance Regulation Will Reshape Lending

The CBUAE’s Open Finance Framework isn’t just another regulatory checkbox. It’s the most ambitious centralized open finance implementation…

The CBUAE’s Open Finance Framework isn’t just another regulatory checkbox. It’s the most ambitious centralized open finance implementation on the planet — and it’s about to fundamentally rewire how lending works in the UAE.

Something extraordinary is happening in UAE financial infrastructure — and most people outside the regulatory perimeter haven’t fully grasped its magnitude yet.

In June 2024, the Central Bank of the UAE issued the Open Finance Regulation, establishing a mandatory, centralized framework for consent-based data sharing and transaction initiation across the entire financial sector. Updated by Circular No. 03/2025 and reinforced by the sweeping CB Law 2025 (Federal Decree-Law No. 6 of 2025), this isn’t a voluntary sandbox experiment It is law. Every CBUAE-licensed bank, insurer, and financial institution must participate.

What makes the UAE’s approach genuinely different from open banking initiatives in the UK, EU, or even Brazil? Three things: a centralized API hub (not fragmented bilateral connections), mandatory participation across banking and insurance from day one, and a CBUAE-backed infrastructure entity — Nebras — operating the entire plumbing. The UAE didn’t copy the playbook. It rewrote it.

This article breaks down what the regulation actually says, how the technology stack works, where implementation currently stands, and most critically — what it means for the future of lending in a country where fintech is projected to reach a $90 billion market by 2031.

The Government Initiatives Driving This

The UAE’s Open Finance framework didn’t emerge in isolation. It’s one of nine pillars within the Financial Infrastructure Transformation (FIT) Programme, launched by the CBUAE in 2023 with a 2026 target for full integration. The programme represents the most comprehensive overhaul of the UAE’s financial plumbing in decades.

KEY INSIGHT

The UAE is the first country globally to implement a consolidated trust framework with a centralized API Hub — meaning a single secure connection can access the entire banking and insurance market. This is architecturally different from the UK’s fragmented approach or the EU’s PSD2 model.

The regulatory backbone was further strengthened in September 2025 when the UAE enacted CB Law 2025, consolidating banking, insurance, payments, and open finance under a single legislative umbrella. Maximum administrative fines were raised to AED 1 billion, and technology platforms facilitating financial services were brought within the CBUAE’s licensing perimeter for the first time. The transition deadline for compliance is September 16, 2026.

Internationally, the UAE has joined Project Aperta, a BIS Innovation Hub initiative to connect domestic open finance infrastructures across jurisdictions — alongside Brazil, the UK, and Hong Kong. For a remittance-heavy economy, this cross-border data portability is strategically significant.

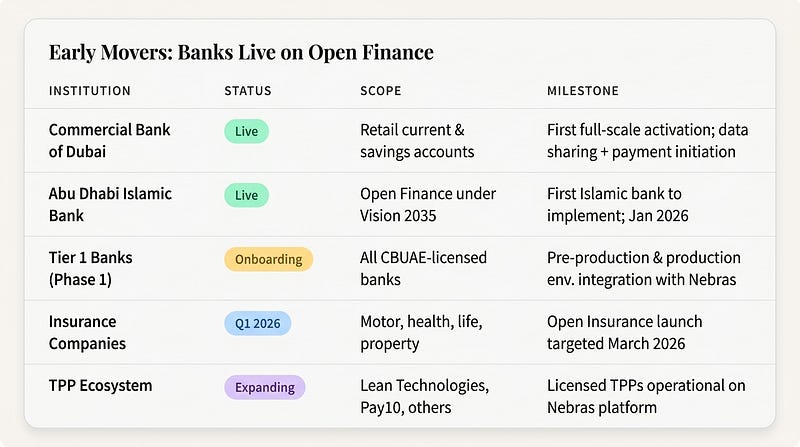

Where Implementation Stands Today

As of Q1 2026, the FIT Programme is 85% complete. The first phase — covering all CBUAE-licensed banks (including foreign branches) and insurance companies — is actively onboarding participants. Several institutions have already gone fully live on the Nebras platform.

Early Movers: Banks Live on Open Finance

The phased approach is deliberate. Banks and insurers form Phase 1. Finance companies, stored value facility providers, and retail payment service providers will follow. Each participant must integrate with the Nebras API Hub via MTLS-secured connections, implement AlTareq consent and authorization flows, and comply with published Open Finance Standards.

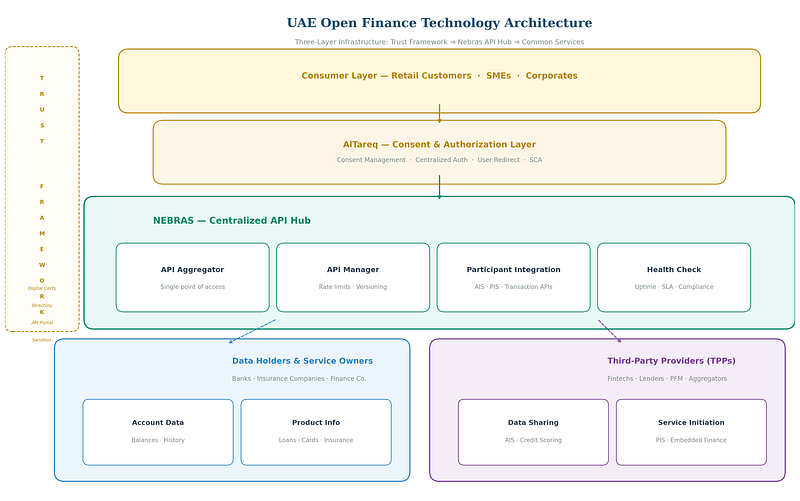

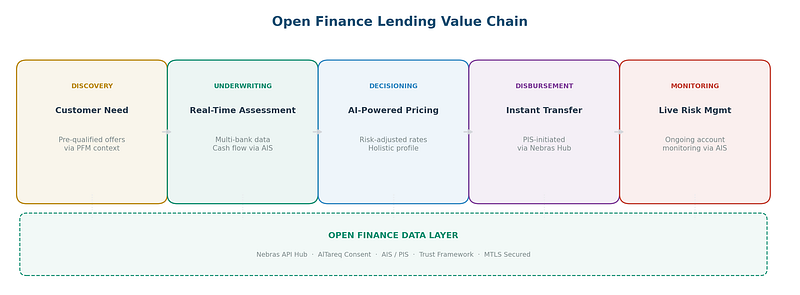

The Technology Stack: How It Actually Works

The UAE’s open finance infrastructure is built on three interlocking layers — the Trust Framework, the API Hub (Nebras), and the Common Infrastructural Services. Together, they form the most tightly integrated open finance platform ever built at national scale.

Core Technology Components

Mutual TLS (MTLS): Bidirectional trust establishment between every participant and the Nebras API Hub. Digital certificates issued via the Trust Framework ensure only authorized entities can communicate.

OAuth 2.0 + Strong Customer Authentication (SCA): Fine-grained consent capture, token issuance, and revocation. SCA is integrated into the AlTareq authorization flow for every data access and payment initiation request.

RESTful API Standards: Standardized Account Information Services (AIS), Payment Initiation Services (PIS), and Transaction APIs published under AlTareq Open Finance Standards. All APIs are versioned, rate-limited, and fully documented.

Microservices Architecture: Modular, scalable design that integrates with both legacy core banking and modern cloud-native systems. API gateway layer (KONG-compatible) handles traffic control, policy enforcement, and caching.

TECHNOLOGY PARTNERS

Core42 (G42 subsidiary) leads infrastructure implementation. Ozone API provides standards-compliant open API platform technology. Raidiam delivers API access management and trust services (proven in Brazil’s open finance). Perfios is empanelled as an official CBUAE system integrator for insurers and lenders.

Commercial & Pricing Model: Nebras operates on a transparent fee model: supplemental licensing plus variable usage fees. API calls are charged between 2.5 and 12.5 fils depending on type. Service Initiation APIs cost 2.5 fils per call, with discounts when paired with Balance or Confirmation of Payee calls within a 2-hour window.

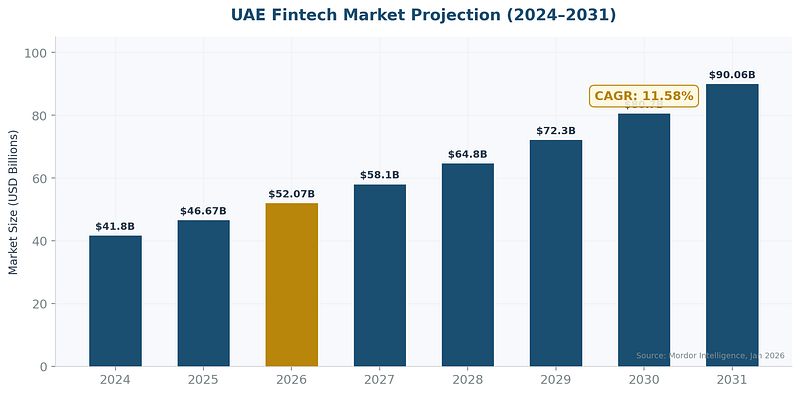

The Market Opportunity: By the Numbers

To understand why open finance matters for lending, you need to grasp the sheer scale of what’s at stake. The UAE’s fintech ecosystem is one of the fastest-growing in the world, and digital lending is its most transformative segment.

How Open Finance Reshapes Lending

The convergence of mandatory data sharing, centralized API infrastructure, and a booming digital economy creates specific, measurable impacts on how credit is originated, underwritten, priced, and distributed in the UAE.

1. Credit Scoring Gets Real Data

Today, a significant portion of UAE residents — particularly expatriates, freelancers, and SMEs — are underserved by traditional credit scoring models that rely heavily on Al Etihad Credit Bureau (AECB) data and salary transfer verification. Open Finance changes this fundamentally. With consent-based access to transaction history, account balances, savings patterns, and product holdings across multiple banks, lenders can build alternative credit models that reflect actual financial behavior. For a country where over 80% of the population are expatriates with fragmented banking relationships, this is transformative.

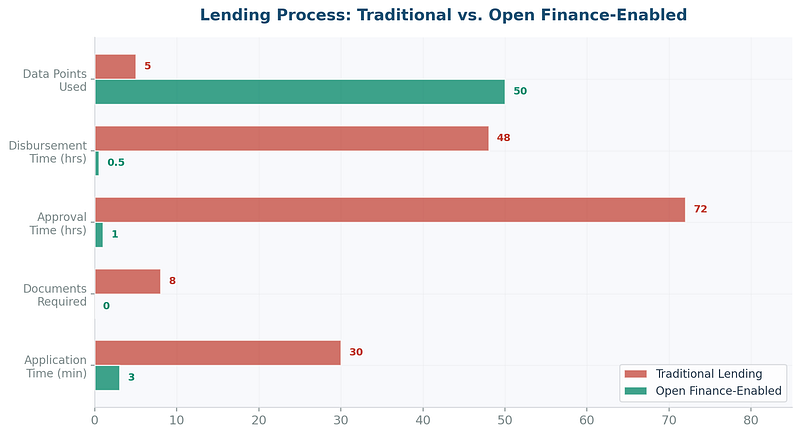

2. Instant Loan Origination

Service Initiation APIs enable lenders to not just assess creditworthiness but to initiate disbursements directly into the borrower’s bank account — without the borrower leaving the lender’s platform. The traditional flow of apply → wait → submit documents → wait → get approved → wait for transfer collapses into a near-real-time experience. Point-of-sale financing tools can now convert retail purchases into installments within seconds.

3. SME Lending Unlocked

SMEs in the UAE have historically faced a credit gap — too small for corporate banking, too complex for consumer products. Open Finance gives lenders visibility into business cash flows, receivables patterns, and multi-bank positions. This enables cash flow-based lending rather than collateral-based lending, unlocking credit for the 15%+ of SMEs actively seeking funding.

4. Embedded Lending Goes Mainstream

The API infrastructure enables non-financial platforms — e-commerce marketplaces, SaaS tools, accounting platforms — to embed lending products directly into their user experience. A logistics company’s dashboard could offer invoice financing. A freelancer platform could offer salary advances. The lending product becomes invisible, contextual, and precisely timed.

Who Benefits — And How

For Consumers

Better Rates Through Data: Lenders with access to the full financial picture can price risk more accurately. Responsible borrowers get lower rates instead of paying a premium because their data was invisible.

Instant, Frictionless Access: No more salary certificates, bank statements, or employer letters. Financial data is shared with consent in seconds — enabling near-instant loan approvals.

True Product Comparison: Aggregator platforms can now pull real product data from across the market. Consumers see genuine best-fit offers instead of whoever has the biggest ad budget.

Control & Consent: Every data share requires explicit, granular consent via AlTareq. Consumers can revoke access at any time. Data sovereignty is baked into the architecture, not bolted on.

For Fintechs & Lenders

Level Playing Field: The centralized API Hub means a single integration gives fintechs access to the entire banking market. No more negotiating bilateral agreements with 50 banks. Plug in once, serve everywhere.

Richer Underwriting: Access to multi-bank transaction data, insurance holdings, and real-time balances enables credit models that were impossible before. Default rates drop. Approval rates rise for good borrowers.

Embedded Distribution: PIS APIs allow disbursement without the borrower leaving the platform. Lending becomes an embedded feature in e-commerce, payroll, accounting, and ERP platforms.

New Revenue Models: The published fee model (2.5–12.5 fils per API call) creates predictable unit economics. Banks can monetize API consumption. Fintechs can build sustainable businesses on transparent infrastructure costs.

What Comes Next

The UAE’s open finance journey is still in its early chapters. The current framework covers banking and insurance, but the CBUAE has signaled broader ambitions. The regulatory trajectory points toward Open Data — extending consent-based data sharing into telecom, utilities, and healthcare. This aligns with the national target of a fully digitized economy by 2026.

For lending specifically, the trajectory is clear: the combination of open finance data, AI-driven underwriting, the Digital Dirham (now legal tender under CB Law 2025), and real-time payment rails will create a credit ecosystem that looks nothing like what exists today. Credit will be contextual, embedded, and priced with unprecedented precision.

THE DIRHAM STORY TAKE

The UAE’s Open Finance Regulation isn’t just a fintech policy. It is industrial strategy. By building centralized, mandatory infrastructure and backing it with institutional capital (Nebras, Al Etihad Payments, Core42), the UAE is constructing the rails on which the next decade of MENA financial innovation will run. Every lender, bank, insurer, and fintech operating in this market needs to understand that the rules of engagement have permanently changed.

Originally published at https://www.linkedin.com.

Comments ()