Inside Wio Bank: How the UAE’s Digital Banking Stack Works

The most important neobank you’ve never heard of just hit AED 61 billion in assets — in three years.

The most important neobank you’ve never heard of just hit AED 61 billion in assets — in three years.

In September 2022, a new bank opened for business in Abu Dhabi. No branches. No legacy systems. No decades of institutional baggage.

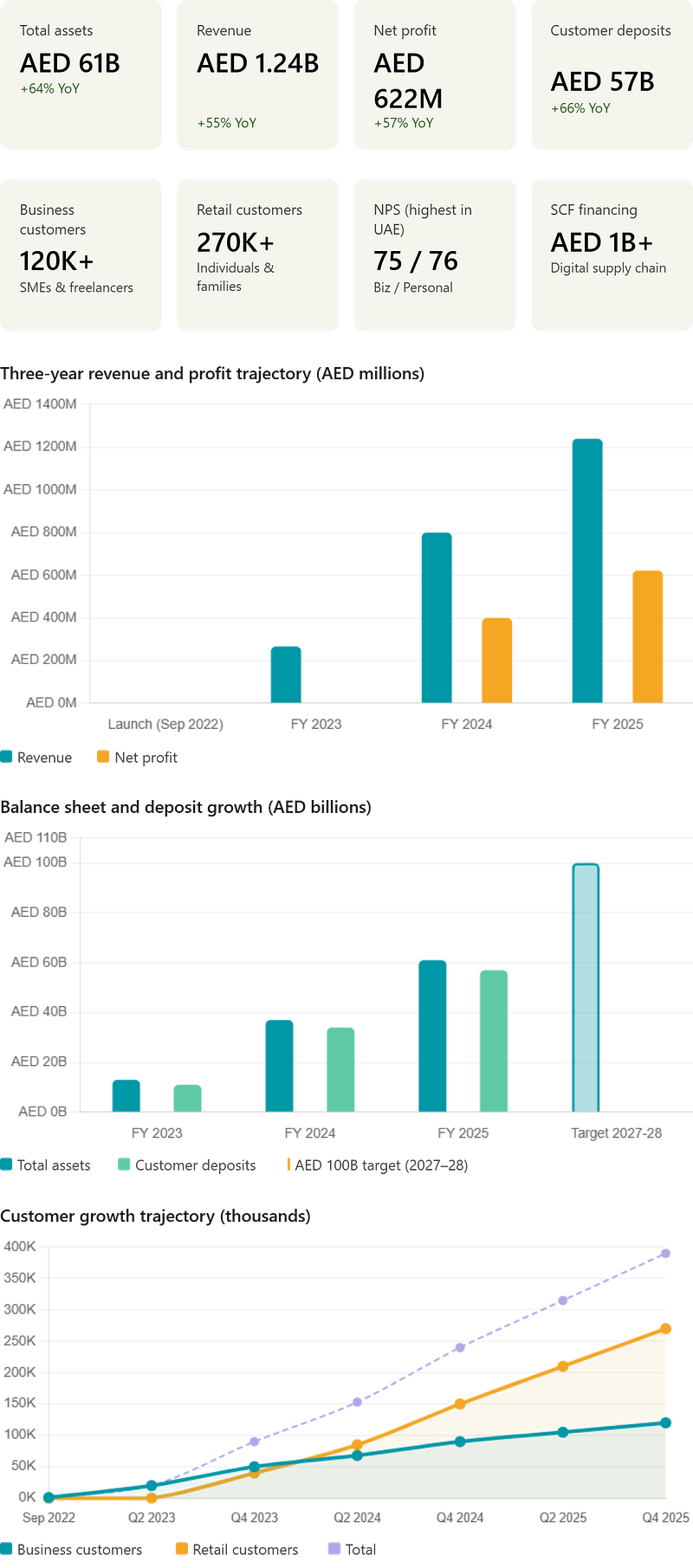

Three years later, Wio Bank PJSC had amassed AED 61 billion ($16.6 billion) in total assets, generated AED 1.24 billion in annual revenues, delivered AED 622 million in net profit, and was serving nearly 390,000 customers — 120,000 businesses and 270,000 individuals.

It achieved the highest Net Promoter Scores in the UAE banking industry: 75 for business and 76 for personal. Its digital supply chain finance platform alone pumped over AED 1 billion in financing into the SME economy. And it’s now preparing to launch Islamic banking in 2026.

This is not a typical neobank story. Wio is something different: a three-sided platform bank built on a composable technology stack, backed by sovereign capital, and operating with a full banking license. Understanding how its digital infrastructure works reveals a blueprint that could reshape banking globally.

The Setup: Why the UAE Was the Right Petri Dish

Before we dissect the technology, context matters. The UAE presented a near-perfect laboratory for this experiment.

The demand side was screaming. Nearly 60% of UAE SMEs remained underserved by traditional banks. Account opening required branch visits, paper-heavy KYC, and multi-week timelines. Meanwhile, 90% of UAE consumers rated digital banking availability as critical — the highest percentage globally, according to Mambu research — and 52% planned to go fully cashless.

The supply side was enabling. The UAE’s Digital Economy Strategy created a regulatory environment that actively encourages platform banking. The Central Bank of the UAE granted Wio a full conventional retail banking license — not a restricted fintech sandbox — allowing it to compete head-to-head with incumbents from day one.

The capital was sovereign. Unlike most neobanks burning through venture capital, Wio launched with AED 2.3 billion in initial capital from ADQ (Abu Dhabi’s sovereign holding company), Alpha Dhabi Holding, e& (formerly Etisalat), and First Abu Dhabi Bank (FAB). This eliminated the fundraising treadmill and provided a virtually unlimited growth runway.

The Stack: A Composable Architecture Masterclass

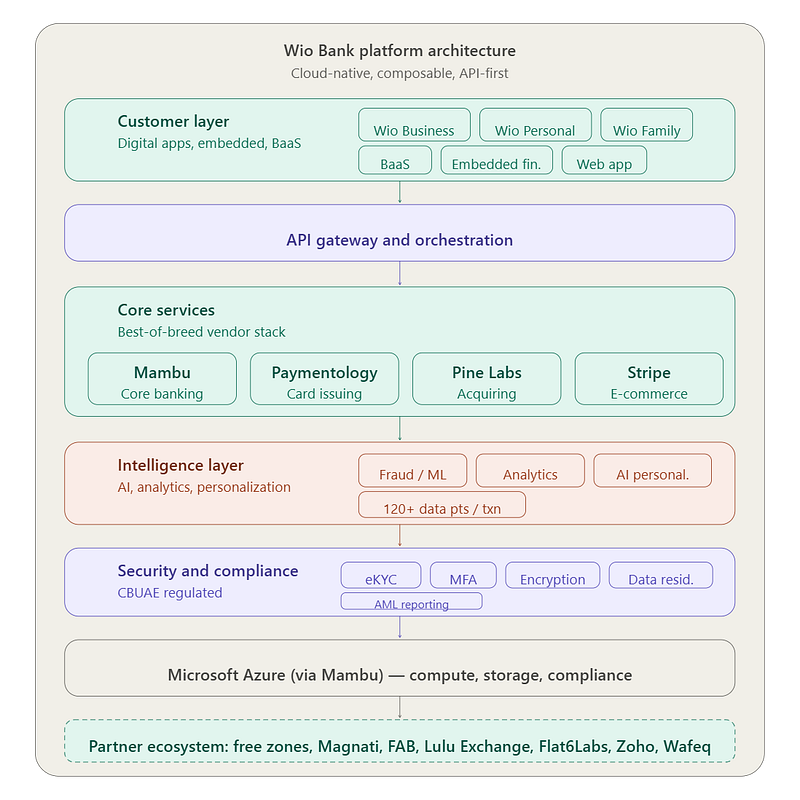

Wio’s technology architecture is a textbook implementation of composable banking. Every functional layer is powered by a best-of-breed provider, orchestrated through standardized APIs, and deployed on shared cloud infrastructure. No single vendor lock-in. No monolithic core. No technical debt from day one.

Here’s how each layer works:

Core Banking: Mambu

At the foundation sits Mambu’s cloud-native, composable core banking platform. Mambu provides the ledger, account management, product configuration, and transaction processing that underpin all operations.

The selection was deliberately architectural. Mambu’s API-first design allows integration with best-of-breed partners across KYC, payments, and analytics — without the rigidity of legacy monolithic cores. Its consumption-based pricing aligned with Wio’s growth path, managing costs efficiently from launch while scaling without re-platforming.

The result: the first Wio Business account went live in just 14 months from inception. The first Wio Personal account followed 11 months later. Both timelines significantly beat industry standards.

As Yatin Parab, Wio’s Chief Product Officer, has described: the bank can configure new products without heavy customization, pivot based on market opportunities, and expand into new segments without significant platform changes.

Cloud Infrastructure: Microsoft Azure

Azure provides compute, storage, networking, and compliance capabilities through Mambu’s partnership. This meets the rigorous data residency and security requirements of UAE regulators while allowing Wio’s engineering teams to focus on product innovation rather than infrastructure management.

The cloud-native approach is directly responsible for an industry-leading cost-to-income ratio. No branches. No hardware. No data centers. Consumption-based pricing that scales with volume.

Card Issuing: Paymentology

Paymentology provides the in-cloud card issuing platform. Through this infrastructure, Wio offers Visa debit cards (physical and virtual), Apple Pay and Google Pay tokenization, card personalization, and multi-currency capabilities.

The critical detail: Paymentology captures 120+ data points per transaction, delivering a real-time data feed of granular customer spending insights. This isn’t just payment processing — it’s a behavioral intelligence engine that continuously informs product development.

Merchant Acquiring: Pine Labs Credit+

Announced in early 2026, this partnership deploys Credit+, an API-first acquiring platform built on microservices architecture. It delivers high transaction throughput, rapid merchant onboarding, and real-time settlement.

This is Wio’s expansion from pure-play issuing into full acquiring — building a two-sided payments network.

E-Commerce Payments: Stripe

Stripe onboarding is embedded directly within the Wio Business app. SME users can create a Stripe account, generate payment links, and start accepting online payments within minutes. Previously, this process required physical in-person onboarding that took days or weeks.

Embedded Finance APIs

Wio’s API layer integrates directly with Zoho Books, Fiskl, and Wafeq — the accounting and taxation platforms UAE SMEs use daily. This enables automated bookkeeping, real-time financial insights, auto-reconciliation, and automated accounts payable.

This layer is what transforms Wio from a banking app into invisible financial infrastructure.

AI and Personalization (2026 Focus)

Wio is accelerating the adoption of artificial intelligence to deliver more personalized financial services, improve customer experience, and support better financial decision-making. This represents the next frontier for the composable stack — layering intelligence on top of infrastructure.

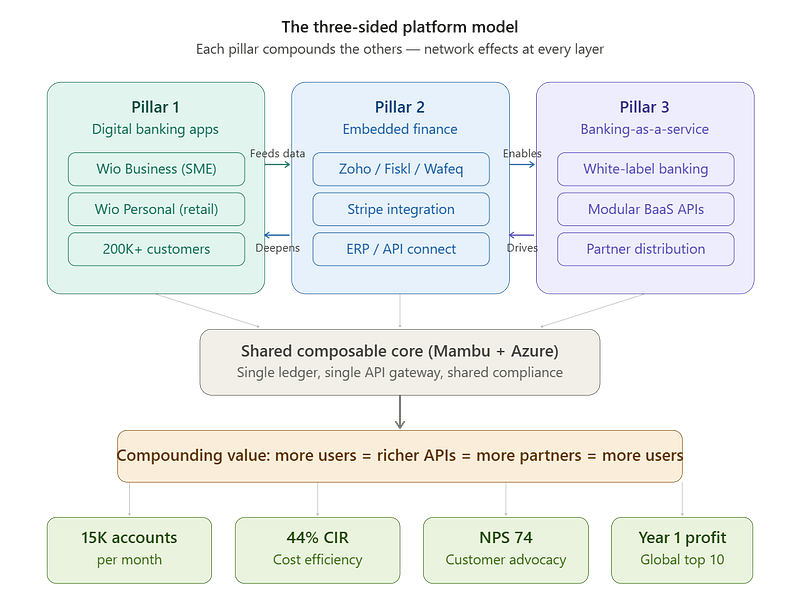

The Model: Three Sides of a Platform

Most neobanks operate on one dimension: they build a digital banking app. Wio operates on three.

Pillar 1: Digital Banking Applications

Three primary apps now serve distinct segments:

Wio Business (launched September 2022) provides SMEs, freelancers, and startups with fully digital account opening, multi-currency accounts, invoicing, WPS payroll compliance, supply chain finance, POS lending, SME credit cards, and savings tools. Over 120,000 businesses now trust Wio as their primary banking partner.

Wio Personal (launched July 2023) serves retail customers with day-to-day banking, smart savings, and competitive interest rates. More than 270,000 individuals have chosen Wio as their primary bank, with 25% moving their salaries to Wio’s payroll platform.

Wio Family (launched Q4 2025) is a fully integrated banking proposition designed to help households manage spending, plan together, and grow their money in one place. It enables financial management across family members including children, supporting financial education. Over 10,000 families adopted it within three months of launch.

Pillar 2: Embedded Finance

Rather than requiring businesses to come to Wio, embedded finance takes banking to where they already operate. Through API integrations with accounting platforms, ERP systems, and taxation tools, financial services are embedded directly into operational workflows. The bank becomes invisible infrastructure.

A standout: Wio’s digital supply chain finance platform delivered over AED 1 billion in financing in 2025 alone, directly improving access to capital for UAE businesses.

Pillar 3: Banking-as-a-Service (BaaS)

Non-banking digital businesses can integrate and white-label Wio’s financial services within their own applications using modular BaaS APIs. Each BaaS partner becomes a distribution channel, creating network effects that compound over time.

Coming in 2026: Wio is developing a Shariah-compliant Islamic banking proposition, subject to regulatory approval. This will enable individual and business customers to manage and grow their money in accordance with their values — extending the platform model into an entirely new market segment.

The flywheel logic: More direct customers generate richer behavioral data, which makes the embedded finance APIs more valuable, which attracts more BaaS partners, which drives more customer acquisition. Each pillar reinforces the others.

The Numbers: A Financial Trajectory That Breaks the Mold

Metric FY 2023 FY 2024 FY 2025 3-Year Change Total Assets ~AED 13B AED 37B AED 61B ~5x Revenue AED 266M AED 800M AED 1.24B ~5x Net Profit AED 2M ~AED 400M AED 622M 311x Customer Deposits AED 11B ~AED 34B AED 57B ~5x Business Customers 50K 90K 120K +140% Retail Customers 40K ~150K 270K +575% NPS (Business) 74 74 75 Highest in UAE NPS (Personal) — — 76 Highest in UAE

Four numbers stand out:

The three-year compounding. From AED 2 million in profit to AED 622 million in three years. From AED 13 billion in assets to AED 61 billion. This isn’t linear growth — it’s exponential, and it’s accelerating.

The deposit base. AED 57 billion in customer deposits, up 66% YoY, represents extraordinary trust in a three-year-old institution. This is core funding, not wholesale — it reflects genuine primary banking relationships.

The revenue mix. A significant share of revenue comes from subscriptions, FX, card interchange, and remittances — not just interest income. This diversification provides resilience against rate cycles and demonstrates product engagement beyond deposit-taking.

The customer economics. With 390,000 customers generating AED 1.24 billion in revenue, the implied revenue per customer is approximately AED 3,180 (~$866) — a strong figure that reflects deep product usage across multiple services.

CEO Jayesh Patel has publicly stated a target of AED 100 billion in assets within two to three years. With the FY2025 trajectory, that target now looks conservative rather than aspirational.

The Competition: A Category of One

Wio’s competitive position is unusual because it competes across multiple dimensions simultaneously:

Against incumbents (FAB, Emirates NBD, ADCB): Wio wins on speed, digital experience, and cost structure. With the expansion into supply chain finance, term loans, and SME credit, the lending gap is closing fast.

Against neobanks (Liv, Mashreq Neo, Zand): Wio wins on architecture sophistication, BaaS capability, sovereign capitalization, and profitability. None of these competitors operate the three-sided platform model or have achieved comparable scale.

Against fintechs (Stripe, Magnati): Wio partners rather than competes, embedding their capabilities into its own platform.

The combination of a full banking license, sovereign backing, composable architecture, three-sided platform model, and now a pathway to Islamic banking places Wio in a category of one within the regional market.

The Partnership Ecosystem as a Moat

Wio’s partnership density is a strategic asset that extends capabilities and distribution:

Free Zone Partnerships with IFZA, ADGM, RAKEZ, and Meydan give Wio access to newly formed businesses at the point of company registration — a customer acquisition channel with near-zero marginal cost.

Technology Alliances with Mambu, Paymentology, Pine Labs, and Stripe form the backbone of the composable stack.

Startup Ecosystem integration through Flat6Labs embeds Wio deeper into the entrepreneurial fabric.

Financial Infrastructure partnerships with FAB, Lulu Exchange, and Magnati provide advanced payment processing, competitive FX, and POS deployment.

Each partnership creates switching costs. Collectively, they form a moat.

Five Lessons from the Wio Playbook

1. Composable architecture beats build-vs-buy.

Assembling best-of-breed components through APIs delivered speed (14 months to first account), agility (features configured not coded), and efficiency (consumption-based pricing). The composable stack is no longer experimental — it is production-grade and demonstrably superior.

2. Sovereign capitalization is a structural advantage.

AED 2.3 billion from sovereign entities eliminated venture fundraising, protected against liquidity constraints, and provided regulatory credibility from inception. This model may be GCC-specific, but it offers a template for government-backed digital banking globally.

3. Platform thinking creates non-linear growth.

Three pillars that compound: direct apps drive acquisition, embedded finance deepens engagement, BaaS creates partner-driven distribution. Each reinforces the others. The FY2025 numbers — 390K customers, AED 57B deposits, AED 1B in supply chain financing — prove the flywheel is spinning.

4. SME-first is a wedge strategy.

Starting with the most underserved segment created maximum marginal value. SME customers are sticky (they integrate payroll, invoicing, accounting, and now supply chain finance) and generate diversified revenue streams. Retail and family banking then leveraged infrastructure already built.

5. Speed is the ultimate competitive advantage.

Fourteen months to first account. Eleven months to retail launch. Profitability in year one. AED 61 billion in three years. Islamic banking on the 2026 roadmap. In a market where incumbents measure launches in quarters and years, Wio’s iteration speed creates a compounding innovation gap.

What Could Go Wrong

Despite the trajectory, several risks merit attention:

Credit risk in the growth phase. As Wio scales lending — supply chain finance, term loans, SME credit, POS lending — credit risk management becomes paramount. Building underwriting capabilities for a fast-growing book is inherently risky, and quality will be tested across economic cycles.

Concentration risk. Growth remains heavily UAE-focused, a market of ~10 million people. While the bank has signaled regional expansion ambitions, execution in new jurisdictions requires new regulatory approvals and market adaptation.

Technology partner dependency. The composable architecture that enables agility also creates dependency on third-party providers. If Mambu, Paymentology, or another critical partner experiences disruptions, Wio faces switching costs.

Islamic banking execution. The planned Shariah-compliant proposition adds product complexity and requires distinct compliance frameworks, scholar oversight, and separate treasury management.

The Bottom Line

Wio Bank is not just building a bank. It is building the operating system for the UAE’s next-generation financial infrastructure — one API at a time.

In three years: AED 61 billion in assets. AED 1.24 billion in revenue. AED 622 million in profit. 390,000 customers. The highest NPS scores in UAE banking. Over AED 1 billion in supply chain financing. A family banking platform. And an Islamic banking launch on the horizon.

The composable architecture, three-sided platform model, and sovereign capitalization have produced results that challenge every assumption about how long it takes to build a profitable, scaled banking institution.

For incumbent banks globally: digital transformation is no longer optional, and Wio has proven the composable path works.

For regulators: progressive licensing catalyzes innovation without compromising prudential standards.

For investors: platform banking — not pure-play digital banking — is the winning model.

The UAE’s first platform bank is, by every measure, already among its most successful. The question now is whether the rest of the industry can catch up.

Data sourced from Wio Bank FY2025 results (March 17, 2026), Mambu case studies, Paymentology partnership announcements, and publicly available financial disclosures.

Comments ()